Choosing between full coverage and liability insurance is one of the most common decisions drivers face.

The difference can significantly impact both your monthly premium and your financial risk.

Many drivers either overpay for coverage they don’t need — or underinsure themselves and face high out-of-pocket costs later.

👉 Compare car insurance quotes here to see how much you could save based on your situation.

Quick Answer: Which Should You Choose?

• If your car is newer, financed, or valuable → full coverage is usually the better choice

• If your car is older and low value → liability may be enough

• If you want maximum protection → full coverage

• If you want the lowest cost → liability only

👉 If you’re unsure, the fastest way to decide is to compare quotes for both options.

In this guide, you’ll learn the real difference between full coverage and liability, when each makes sense, and how to choose the best option for your situation.

What Is Liability Insurance?

What Is Liability Car Insurance?

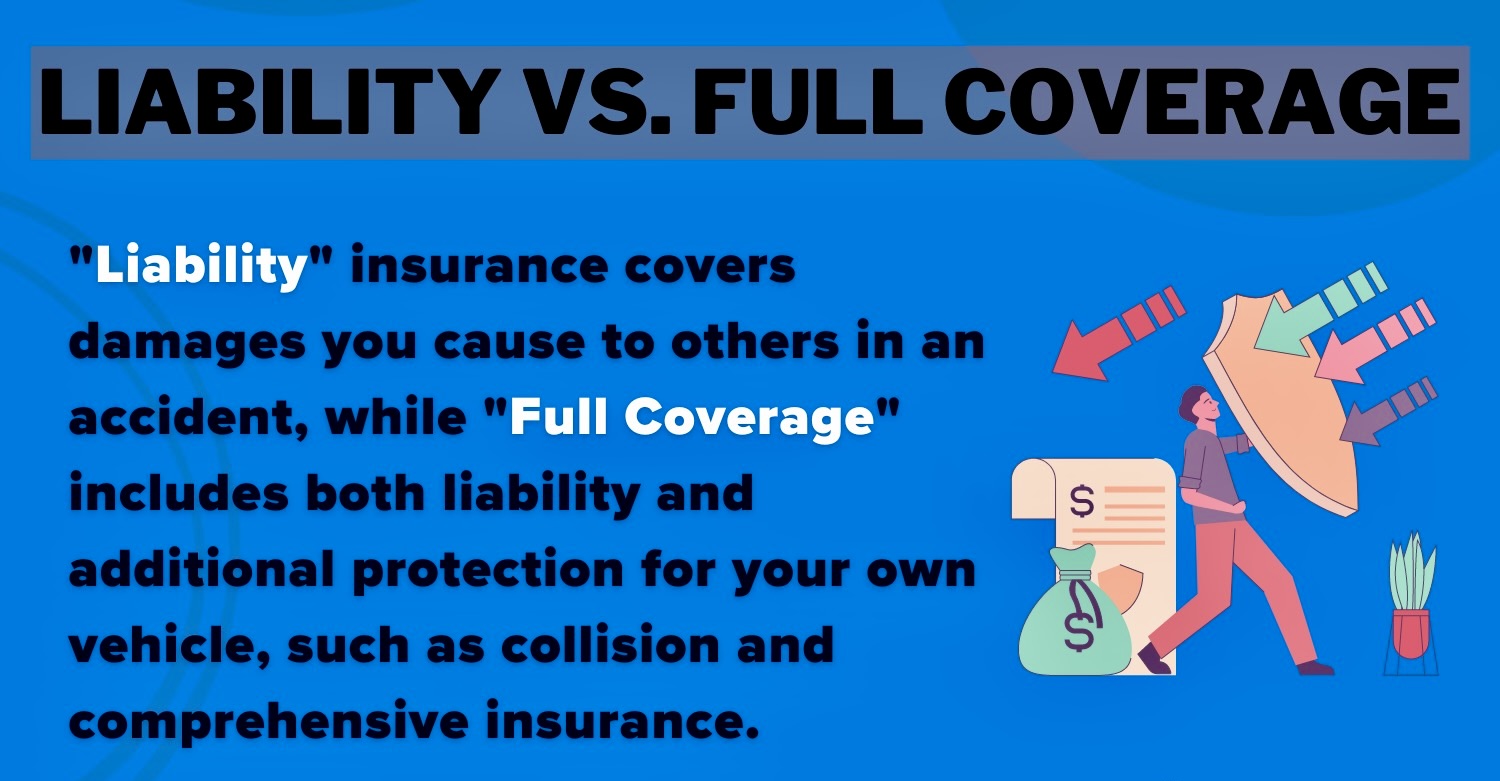

Liability insurance is the minimum coverage required in most states. It only covers damage you cause to other people. It is designed to protect other people, not your own vehicle.

This means if you are at fault in an accident, your insurance will pay for the damage you cause to others, but not your own car.

Because of this, liability insurance is usually the cheapest option, but it also carries more financial risk.

- Bodily injury (others)

- Property damage (others)

It does NOT cover:

- Your own car damage

- Theft or vandalism

- Weather-related damage

This is why liability insurance is cheaper — it provides limited protection.

What Is Full Coverage ?

What Is Full Coverage Car Insurance?

Full coverage is not a single policy, but a combination of multiple coverages. It offers a higher level of protection by including both collision and comprehensive insurance.

This means your own vehicle is covered in situations like accidents, theft, vandalism, or natural disasters.

While it costs more, it provides peace of mind, especially for newer or more valuable vehicles.

- Liability insurance

- Collision coverage

- Comprehensive coverage

This means it covers both:

- Damage to others

- Damage to your own vehicle

👉 Learn how coverage affects your cost:

→ Best Car Insurance Coverage in the USA: What You Really Need in 2026

📊 Full Coverage vs Liability (Key Differences)

Full Coverage vs Liability: Key Differences

| Feature | Liability | Full Coverage |

|---|---|---|

| Covers others | ✔ | ✔ |

| Covers your car | ❌ | ✔ |

| Cost | Lower | Higher |

| Required by law | ✔ | ❌ |

The difference between these two options is not just about cost, but also about financial risk.

Choosing liability may save money each month, but it could lead to significant out-of-pocket expenses after an accident.

Full coverage, on the other hand, reduces that risk but comes at a higher monthly cost.

Before choosing a policy, drivers should also think about which car insurance coverage fits their vehicle, budget, lender requirements, and risk level.

Cost Difference

How Much More Does Full Coverage Cost?

Full coverage is significantly more expensive.

On average:

- Liability: $80–$120/month

- Full coverage: $150–$250/month

However, the price varies by driver and provider.

Insurance cost differences can vary widely depending on your profile.

Factors such as your driving history, credit score, and location can significantly affect how much more you pay for full coverage.

This is why comparing quotes is essential — the price gap may be smaller than you expect.

Real Cost Comparison Over Time

Many drivers focus only on the monthly premium, but the real cost is what you pay over time.

For example:

- Liability: $100/month → $1,200/year

- Full Coverage: $200/month → $2,400/year

The difference is $1,200 per year.

However, one accident could cost several thousand dollars in repairs. Liability coverage leaves you exposed if your car is damaged.

👉 Learn how deductibles affect your premium in this guide.

This is why choosing the right coverage is not just about saving money, but also about managing financial risk.

Which One Should You Choose?

Should You Choose Full Coverage or Liability?

Choose liability if:

- Your car is older

- You want the lowest monthly cost

Choose full coverage if:

- Your car is new or valuable

- You want full protection

The best choice depends on your financial situation and risk tolerance.

Here are some real-life scenarios to help you decide:

If your car is older and has a low market value, paying for full coverage may not be worth it.

If your car is new or financed, full coverage is usually required and strongly recommended.

If you rely on your car daily and cannot afford unexpected repair costs, full coverage may be the safer option.

However, if your goal is to minimize monthly expenses and you can handle potential repair costs, liability may be enough.

When Liability Insurance Makes More Sense

Liability insurance is often the better choice in certain situations.

If your car is older and has a low market value, paying for full coverage may not be worth the extra cost.

For example, if your car is worth $2,000 and full coverage costs you an extra $1,000 per year, the math may not make sense.

In this case, liability insurance can help you save money while still meeting legal requirements.

However, you should only choose liability if you can afford to repair or replace your vehicle out of pocket if needed.

When Full Coverage Is the Better Choice

Full coverage is usually the better option if your vehicle is newer or financed.

If you have a car loan or lease, lenders typically require full coverage to protect their investment.

It is also a safer choice if you rely heavily on your car for daily commuting or work.

In the event of an accident, full coverage can prevent large unexpected expenses.

While it costs more each month, it provides financial protection and peace of mind.

See real price differences based on your profile. Takes about 2 minutes.

Understanding the Risk Difference

The biggest difference between liability and full coverage is financial risk.

With liability insurance, you take on the risk of paying for your own vehicle damage.

With full coverage, the insurance company shares that risk.

If you cannot afford unexpected repair costs, choosing liability could be risky.

On the other hand, if you are financially prepared, liability may be a cost-saving option.

Common Mistakes

Common Mistakes to Avoid

- Choosing liability just to save money

- Overpaying for full coverage on an old car

- Not comparing quotes

👉 Many drivers make decisions without checking actual prices.

Many drivers choose coverage based only on price without considering long-term risk.

Others overpay for full coverage even when their vehicle is no longer worth it.

Understanding when to adjust your coverage is key to avoiding unnecessary expenses.

💡 Not sure which coverage is best for you?

Compare quotes from top companies and see real prices based on your situation.

FAQs

Is full coverage worth it?

It depends on your car value and financial situation.

Can I switch from full coverage to liability?

Yes, you can adjust your policy anytime.

Is liability enough?

Only if you can afford to repair or replace your own car.

Final Thoughts: Which Is Better?

There’s no single answer — it depends on your car, your budget, and your risk tolerance.

But one thing is consistent:

👉 Insurance prices vary widely between companies.

Comparing quotes is the simplest way to see which option actually makes sense for your situation.

👉 Compare quotes from multiple providers before choosing your coverage.

Sources

Insurance Information Institute (III)

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.