What deductible should you choose for your car insurance?

Many drivers pick a deductible without fully understanding how it affects their premium — and this mistake can cost hundreds of dollars every year.

👉 The fastest way to see how different deductibles affect your price is to compare quotes from multiple companies.

In simple terms, your deductible is the amount you pay out of pocket before your insurance covers the rest.

Choosing the right deductible is a balance between saving money on your monthly premium and managing your financial risk in case of an accident.

In this guide, you’ll learn exactly how deductibles work, how they affect your insurance cost, and how to choose the best option for your situation.

🔍 What Is a Car Insurance Deductible?

What Is a Car Insurance Deductible?

A deductible is the amount you agree to pay before your insurance company pays for a covered claim.

For example, if you have a $1,000 deductible and your repair costs $3,000, you will pay $1,000 and your insurance will cover the remaining $2,000.

Deductibles typically apply to:

- Collision coverage

- Comprehensive coverage

They do not usually apply to liability insurance, which covers damage you cause to others.

Understanding this difference is important, because your deductible only affects certain parts of your policy, not all of it.

👉 Not sure what coverage you need?

Read: Full Coverage vs Liability Insurance

Not sure whether you should choose a high or low deductible?

👉 Our full guide:

Read: Deductible vs Premium: How to Choose the Best Option

💰 How Deductibles Affect Your Premium?

How Does Your Deductible Affect Your Insurance Premium?

Your deductible has a direct impact on how much you pay each month.

- Higher deductible → Lower premium

- Lower deductible → Higher premium

This happens because a higher deductible means you are taking on more financial risk, so the insurance company charges you less.

On the other hand, a lower deductible means the insurer takes on more risk, which increases your premium.

For many drivers, adjusting the deductible is one of the fastest ways to reduce monthly insurance costs.

👉 Want to see how much you could save?

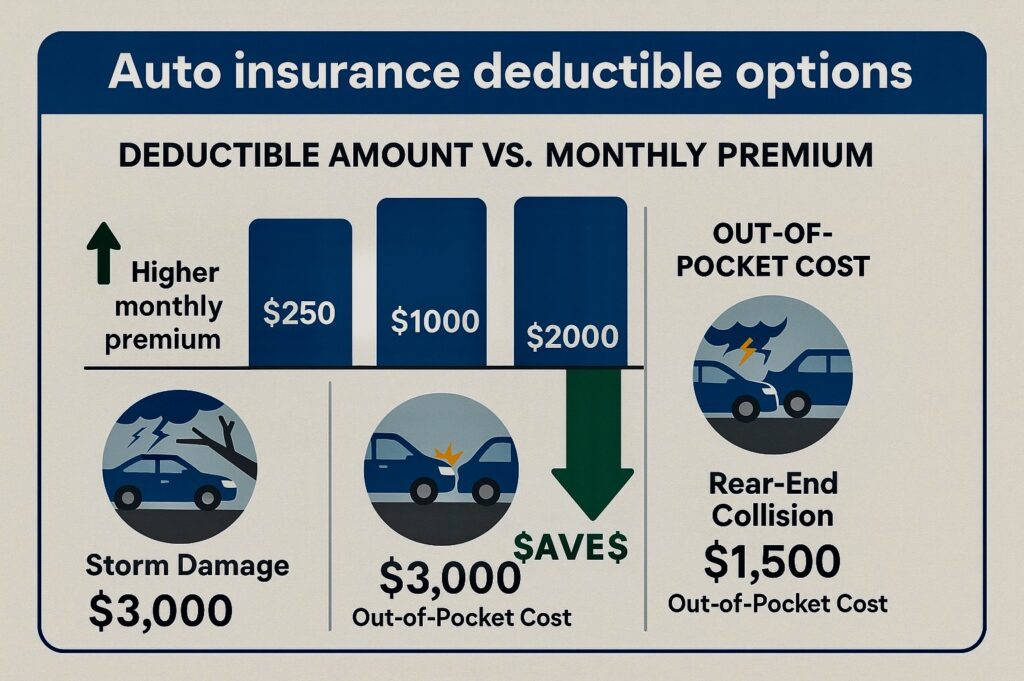

📊 Example of Deductible Impact

Example: How Deductible Changes Your Cost

Here’s a simple example:

| Deductible | Monthly Premium |

|---|---|

| $500 | $180 |

| $1,000 | $140 |

| $2,000 | $110 |

Over a year, the difference can be significant.

Choosing a higher deductible could save you hundreds of dollars annually.

However, you must be prepared to pay that higher amount if you file a claim.

👉 That’s why comparing quotes is essential:

🧠 How to Choose the Right Deductible

How to Choose the Right Deductible

Choosing the right deductible depends on your financial situation and risk tolerance.

Here are a few key factors to consider:

1. Your Emergency Savings

If you have enough savings to cover a higher deductible, you can safely choose a higher amount and lower your premium.

2. Your Driving Habits

If you drive frequently or in high-risk areas, a lower deductible may be safer.

3. Your Vehicle Value

For older cars, a high deductible may make more sense since the car’s value is lower.

4. Your Monthly Budget

If your goal is to reduce monthly expenses, increasing your deductible can help.

There is no one-size-fits-all answer — the best choice depends on your personal situation.

⚖️ Low vs High Deductible (Pros and Cons)

Low vs High Deductible: Pros and Cons

Low Deductible (e.g., $250–$500)

Pros:

- Lower out-of-pocket cost after an accident

- Less financial stress in emergencies

Cons:

- Higher monthly premium

High Deductible (e.g., $1,000–$2,000)

Pros:

- Lower monthly premium

- Long-term savings

Cons:

- Higher upfront cost if you file a claim

Understanding these trade-offs is essential for making a smart decision.

🧾 When a High Deductible Makes Sense

When Should You Choose a High Deductible?

A high deductible is usually a good choice if:

- You have emergency savings

- You want to lower your monthly premium

- Your car is older or less valuable

Many drivers choose higher deductibles to save money over time.

However, this only works if you can afford the higher cost in case of an accident.

🚗 When a Low Deductible Is Better

When Is a Low Deductible the Better Option?

A low deductible may be the better choice if:

- You cannot afford a large unexpected expense

- You drive frequently in high-risk conditions

- You rely heavily on your car

In these cases, paying a higher monthly premium may be worth the added protection.

💡 Not sure which deductible is best for you?

Compare quotes from top insurers and see how different options affect your price.

Common Mistakes to Avoid

Common Deductible Mistakes to Avoid

Avoid these common mistakes:

- Choosing the lowest deductible without considering cost

- Selecting a high deductible without having savings

- Not reviewing your deductible regularly

- Ignoring how deductible affects long-term cost

Many drivers overpay simply because they don’t adjust their deductible when their situation changes.

❓ FAQs

FAQs About Car Insurance Deductibles

What is the best deductible amount?

There is no single best amount. It depends on your finances and risk tolerance.

Is a $1,000 deductible a good choice?

For many drivers, $1,000 is a good balance between savings and risk.

Can I change my deductible later?

Yes, you can update your deductible at any time.

Does a higher deductible always save money?

Usually yes, but only if you don’t file frequent claims.

Choose the Right Deductible and Start Saving Today

Your deductible plays a major role in how much you pay for car insurance.

By choosing the right amount, you can reduce your premium while still protecting yourself financially.

Sources

Insurance Information Institute (III)

👉 Take 2 minutes to compare quotes and find the best option for your situation.

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.