Introduction

Choosing between a higher deductible or a lower premium is one of the most important decisions when buying car insurance.

Make the wrong choice, and you could end up paying hundreds more every year—or thousands after an accident.

👉 In this guide, you’ll learn:

- What deductible and premium really mean

- How they affect your total cost

- Which option saves you more money

- How to choose based on your situation

👉 Want to see your real price instantly?

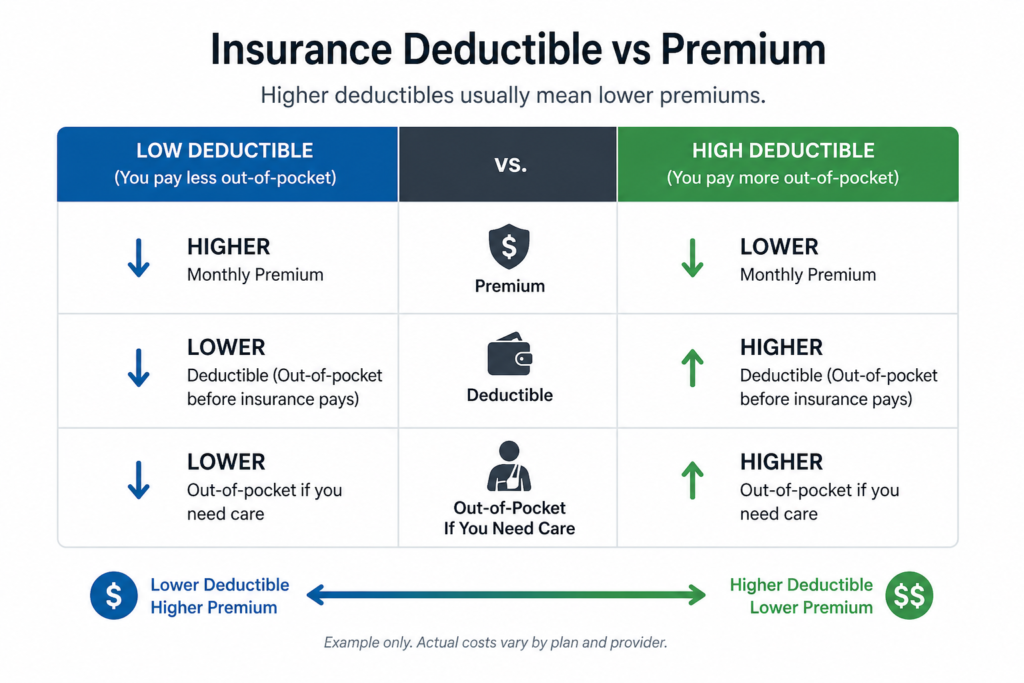

What Is a Deductible?

A deductible is the amount you pay out of pocket before your insurance covers the rest.

Example:

- Deductible: $1,000

- Accident cost: $3,000

👉 You pay $1,000

👉 Insurance pays $2,000

The higher your deductible, the more risk you take—but the less you pay monthly.

What Is a Premium?

Your premium is the amount you pay to keep your insurance active.

You can pay:

- Monthly

- Or in full

👉 Lower deductible = higher premium

👉 Higher deductible = lower premium

Deductible vs Premium: How They Work Together

👉 There’s an inverse relationship between deductible and premium:

- Increase your deductible → your premium goes down

- Decrease your deductible → your premium goes up

👉 You are choosing between:

- Paying more now (premium)

- Or paying more later (deductible)

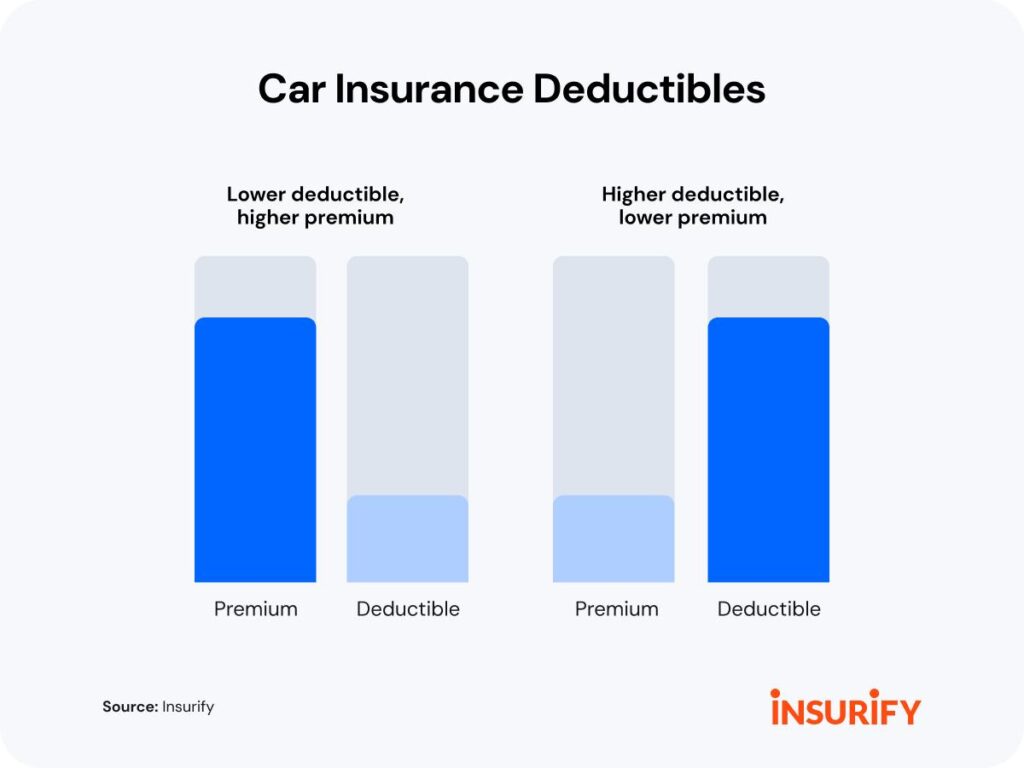

Real Cost Comparison: Deductible vs Premium

To clearly understand the impact of deductible vs premium, let’s look at a realistic long-term scenario.

Imagine two drivers in the USA choosing different insurance plans:

Option A: Low Deductible Plan

- Deductible: $500

- Monthly Premium: $180

- Annual Cost: $2,160

Option B: High Deductible Plan

- Deductible: $1,500

- Monthly Premium: $110

- Annual Cost: $1,320

At first glance, Option B saves $840 per year, which seems like the better deal.

However, the real difference appears when you consider risk.

Scenario 1: No Accident (3 Years)

- Option A total cost: $6,480

- Option B total cost: $3,960

👉 Option B saves $2,520 over 3 years.

Scenario 2: One Accident

Assume repair cost = $3,000

- Option A: Pay $500 → Insurance covers rest

- Option B: Pay $1,500 → Insurance covers rest

👉 Option B costs $1,000 more out-of-pocket

What This Means

Choosing between deductible and premium is a trade-off:

- Higher deductible → Lower monthly cost but higher risk

- Lower deductible → Higher monthly cost but lower financial shock

Insurance companies charge lower premiums for higher deductibles because you take on more risk yourself

👉 Best Choice Based on Situation

- Choose high deductible if:

- You rarely drive

- You have emergency savings

- You want lower monthly expenses

- Choose low deductible if:

- You want predictable costs

- You can’t afford large sudden expenses

- You drive frequently

If you want to lower your overall cost, check our guide on how to save money on car insurance in the USA.

Break-Even Point: When Does a High Deductible Pay Off?

This is the most important concept most drivers ignore.

Let’s say:

- You save $600/year with a high deductible

- But pay $750 more in an accident

👉 You need to avoid accidents for about 1.25 years to come out ahead.

What Most Drivers Get Wrong About Deductibles

Many drivers choose a deductible based only on what feels affordable monthly.

But this is a mistake.

👉 The real question is not:

“How much can I pay per month?”

👉 It should be:

“How much can I afford if an accident happens tomorrow?”

Example:

- You choose a $1,000 deductible to save $50/month

- You get into an accident next month

👉 You now need $1,000 immediately

Reality Check:

If you don’t have enough savings to cover your deductible:

👉 A high deductible can become a financial problem

👉 That’s why experts recommend:

- Only choose a high deductible if you can comfortably pay it anytime

Simple Rule:

- No accidents → high deductible wins

- Frequent claims → low deductible wins

👉 Want to find your best option instantly?

Pros and Cons of Each Option

High Deductible

Pros:

- Lower monthly premium

- Saves money over time

Cons:

Financial risk if you don’t have savings

Higher out-of-pocket cost after an accident

Low Deductible

Pros:

- Lower cost after a claim

- More financial protection

Cons:

- Higher monthly premium

- Higher total cost over time

How to Choose the Right Deductible (Step-by-Step)

Here’s a simple method:

Step 1: Check Your Emergency Savings

- Less than $500 → choose low deductible

- $500–$1,500 → medium deductible

- $1,500+ → high deductible

Step 2: Evaluate Your Driving Risk

Ask yourself:

- Do you drive daily?

- Do you drive in heavy traffic?

- Have you had accidents before?

👉 Higher risk = lower deductible

Step 3: Compare Real Quotes

Prices vary a lot depending on:

- Your location

- Your driving history

- Your credit score

👉 The best way to decide:

Who Should Choose a High Deductible?

A high deductible is best if you:

- Are a safe driver

- Rarely file claims

- Have emergency savings

- Want to minimize long-term cost

👉 This is the most cost-efficient strategy for disciplined drivers.

Who Should Choose a Low Deductible?

A low deductible may be better if you:

- Are a new or high-risk driver

- Don’t have savings for emergencies

- Want predictable costs

- Drive frequently in high-risk areas

👉 This option reduces financial stress after accidents.

Smart Strategy (What Most People Should Do)

Here’s the best approach:

- Compare multiple insurance quotes

- Choose the lowest premium

- Adjust deductible based on your risk tolerance

👉 Start here:

How This Connects to Your Total Insurance Cost

Your deductible is just one part of your total cost.

👉 To reduce your premium even further, you can read this guide for more details.

Does Credit Score Affect Your Premium?

Yes-your credit score can significantly impact your insurance rate.

Drivers with higher credit scores usually pay less.

Not Sure What a Deductible Is?

If you’re still confused about how deductibles work, check out our guide on What a Deductible Is?

🔥 Quick Decision: High or Low Deductible?

- Want to save the most money long-term? → Choose a high deductible

- Want lower risk after an accident? → Choose a low deductible

- Have $1,000+ in savings? → High deductible is usually better

- Living paycheck to paycheck? → Low deductible is safer

👉 Still unsure?

Final Verdict: Which One Should You Choose?

- Want lower monthly payments → choose a higher deductible

- Want lower risk after an accident → choose a lower deductible

👉 The best choice depends on your financial situation and risk tolerance.

For most drivers who have emergency savings, a high deductible is the better financial choice.

Common Deductible Options in the U.S.

Most insurance companies offer these choices:

- $250

- $500

- $1,000

- $2,000

Typical Strategy:

- $500 → balanced choice

- $1,000 → most common for saving money

👉 The higher you go, the more you save—but the more risk you take.

Conclusion:

There is no one-size-fits-all answer.

But one thing is clear:

👉 Understanding the relationship between deductible and premium can save you hundreds or even thousands of dollars over time.

If you have savings and rarely file claims → choose a high deductible.

If you don’t have emergency savings → choose a low deductible.

Don’t guess your rate—compare it.

👉 Prices vary widely based on your profile and location.

👉 Check your real price now:

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.