Introduction

Looking for no down payment car insurance?

You’re not alone. Many drivers want to start coverage without paying a large upfront cost.

But here’s the truth:

👉 Most “no down payment” insurance plans don’t actually mean $0 upfront.

In this guide, you’ll learn:

- What “no down payment” really means

- Whether it’s legit or misleading

- How to find the lowest upfront cost

- Smart ways to save money

Can You Really Get Car Insurance with $0 Down?

Many drivers search for “no down payment car insurance” expecting to pay nothing upfront.

👉 In reality, true $0 down policies are extremely rare.

Most insurance companies require at least:

- A first month payment

- Or a small deposit

Why $0 Down Is Rare

Insurance companies take risk immediately when coverage starts.

Without any payment:

- Drivers could cancel instantly

- Insurers would lose money

👉 That’s why most “no down payment” plans still require a small upfront cost.

👉 Want to see your real price instantly?

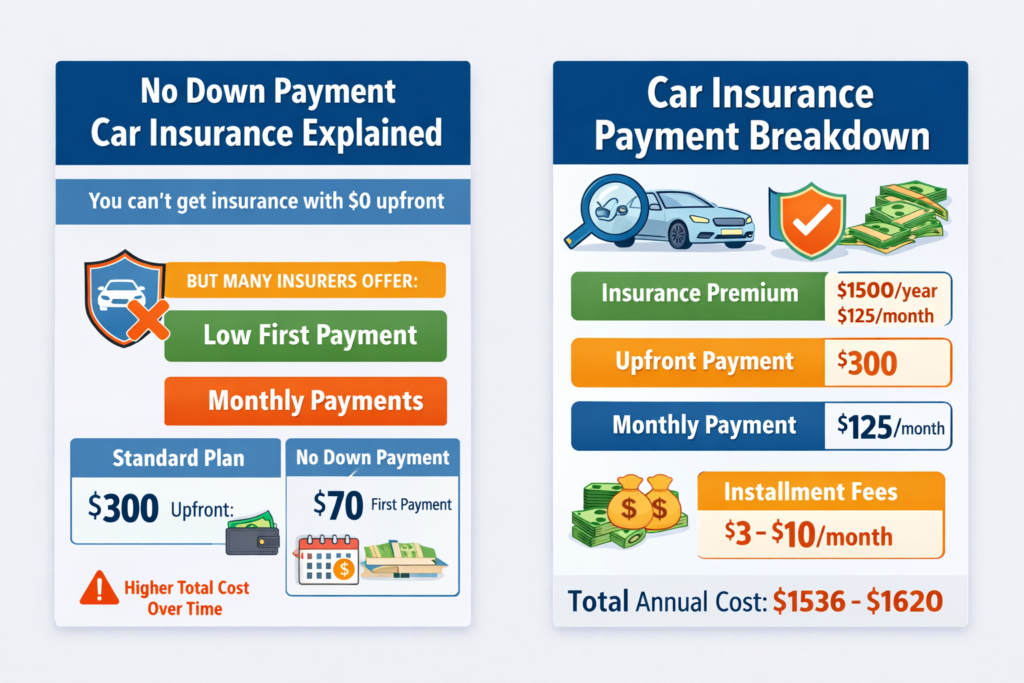

What Is No Down Payment Car Insurance?

“No down payment” car insurance usually means:

👉 You don’t pay a large lump sum upfront

👉 Instead, you start with a small first payment and continue monthly

Important:

In most cases:

- You still pay something upfront

- It’s just lower than a typical deposit

👉 Example:

- Standard plan: $300 upfront

- “No down payment” plan: $80 first payment

Why Insurance Companies Require Upfront Payment

Insurance companies take risk the moment your policy starts.

They require upfront payment to:

- Reduce risk of missed payments

- Confirm commitment

- Cover initial administrative costs

👉 That’s why true $0 insurance is extremely rare.

Best Insurance Companies for Low Down Payment Plans

Best Insurance Companies for Low Down Payment Plans

While true no down payment car insurance does not exist, some insurers are known for offering relatively low upfront payments and flexible monthly billing options.

Progressive

Progressive is often one of the first companies drivers compare when looking for affordable monthly insurance plans. Many drivers with imperfect records, including those with accidents or violations, may find competitive payment options through Progressive. The company also offers online quotes and flexible billing schedules in many states.

GEICO

GEICO is frequently known for competitive pricing, especially for drivers with clean records. Depending on your location and coverage level, GEICO may allow you to start coverage with a relatively low initial payment and spread the remaining premium across monthly installments.

State Farm

State Farm is one of the largest auto insurers in the United States. Drivers who already have homeowners, renters, or life insurance with State Farm may qualify for bundling discounts that reduce both upfront and long-term insurance costs.

Dairyland

Dairyland specializes in serving higher-risk drivers. If you have a DUI, SR-22 requirement, or a limited insurance history, Dairyland may provide coverage options when other companies charge higher initial premiums.

National General

National General often offers flexible payment plans and coverage options for drivers seeking lower upfront costs. Availability and pricing vary by state, making comparison shopping especially important.

Because rates and payment plans vary significantly by company, comparing multiple quotes is often the best way to reduce your initial payment while still maintaining adequate coverage.

Is No Down Payment Car Insurance Legit?

👉 Yes—but it’s often misunderstood

What’s real:

- Some insurers offer low initial payment plans

- Flexible billing options exist

What’s misleading:

- “$0 down” often still requires a first payment

- Total cost may be higher over time

👉 Bottom line:

You’re not avoiding payment—you’re spreading it out

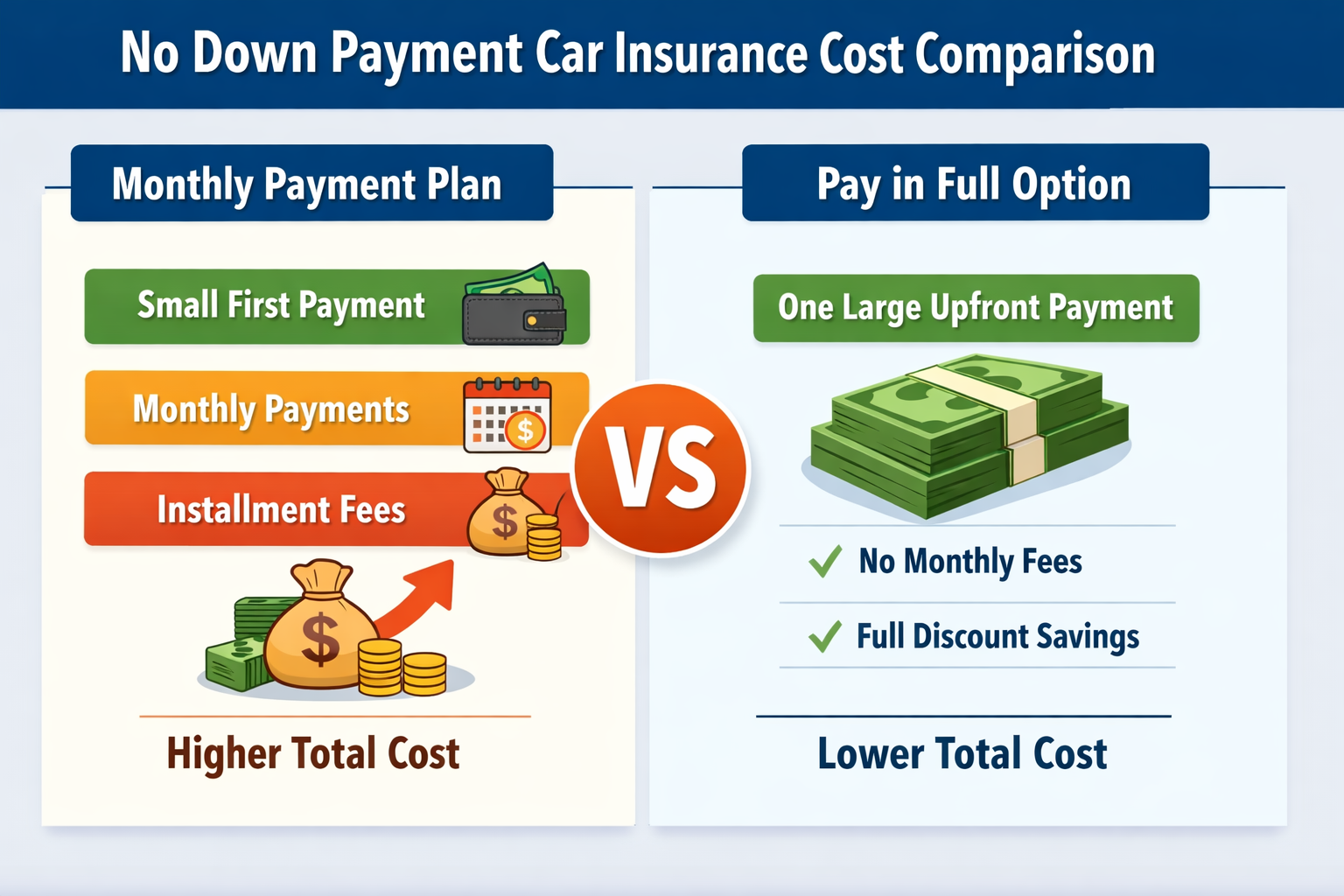

No Down Payment vs Pay in Full

| Option | Upfront Cost | Total Cost | Best For |

|---|---|---|---|

| Pay in Full | High | Lowest | Saving money |

| No Down Payment | Low | Higher | Cash flow flexibility |

👉 If your goal is the lowest overall cost, paying upfront is usually the better option—learn more in our guide to pay in full car insurance.

Pros and Cons

Pros

- Low upfront cost

- Easier to start coverage

- Better for tight budgets

Cons

- Higher total premium

- Monthly fees may apply

- Risk of missed payments

👉 Monthly plans often include extra fees

How Much Is a Typical Down Payment?

The amount you pay upfront depends on your profile.

Here’s a general range:

- Low-risk drivers: $50 – $150

- Average drivers: $100 – $300

- High-risk drivers: $300+

Key Insight:

👉 The higher your risk, the higher your upfront payment.

Factors that affect it include:

- Driving record

- Credit score

- Coverage level

Who Should Consider No Down Payment Insurance?

This option may work for you if:

- You don’t have enough savings

- You need immediate coverage

- You prefer smaller payments

👉 Best for short-term flexibility

Who Should Avoid It?

You may want to avoid it if:

- You can afford to pay in full

- You want the lowest total cost

- You are financially stable

👉 In most cases:

Paying more upfront saves money long-term.

Real-Life Example: Comparing Low Down Payment Insurance Options

Imagine a California driver who needs insurance immediately but has limited cash available. One insurer may require a $250 upfront payment with lower monthly premiums, while another may advertise a $50 down payment but charge significantly higher monthly rates.

At first glance, the lower upfront payment appears to be the better deal. However, over a six-month policy period, the total cost may actually be much higher.

This is why drivers should focus on the total policy cost rather than only the initial payment. Comparing multiple quotes allows you to balance affordability today with lower long-term expenses.

The best insurance option is often not the one with the lowest down payment, but the one with the lowest overall cost.

How to Get the Lowest Down Payment

Here are proven strategies:

1. Compare Multiple Quotes

Prices vary significantly between insurers.

👉 Start here:

2. Adjust Your Coverage

Lower coverage = lower upfront payment

But be careful not to underinsure yourself.

3. Increase Your Deductible

Higher deductible → lower premium

Increasing your deductible can significantly lower your premium—see how it works in deductible vs premium.

4. Improve Your Credit Score

Better credit → lower insurance rates

Your credit score can impact how much you pay, so it’s worth understanding how credit score affects car insurance rates.

Hidden Costs to Watch Out For

Many drivers focus only on upfront cost—but ignore total cost.

Monthly Payments vs Low Down Payment: What’s the Difference?

Many drivers confuse these two options.

Monthly Payment Plan

- Pay a deposit

- Then pay monthly

- Includes installment fees

Low Down Payment Plan

- Smaller upfront cost

- Still includes monthly payments

- Often slightly higher premium

👉 In most cases:

Both options cost more than paying in full.

No Down Payment Car Insurance in California

California drivers often search for no down payment car insurance because insurance costs in many parts of the state are among the highest in the country.

In reality, California insurance companies generally require some form of initial payment before coverage becomes active. The amount can vary depending on several factors:

- ZIP code

- Driving record

- Vehicle type

- Coverage limits

- Insurance history

Drivers with clean records and good credit-related insurance factors may qualify for lower upfront payments and more favorable monthly billing options.

Drivers with recent accidents, lapses in coverage, or DUI convictions may face higher initial costs.

Because California premiums vary significantly from city to city, comparing quotes from multiple companies is often the fastest way to identify affordable coverage with a lower initial payment requirement.

Why “No Down Payment” Can Cost More Over Time

While low upfront cost sounds attractive, it often leads to higher total payments.

Monthly plans usually include:

- Installment fees

- Higher premiums

- Less discount eligibility

Over time, this can cost you significantly more than paying upfront.

👉 That’s why it’s important to compare total cost—not just the first payment.

Common hidden fees:

- Installment fees

- Late payment penalties

- Policy reinstatement fees

👉 These can add up quickly over time.

Smart Strategy (What Most Drivers Should Do)

Here’s the best approach:

- Compare quotes first

- Choose the lowest premium

- Decide payment plan based on your cash flow

👉 Start here:

Common Myths About No Down Payment Insurance

Myth 1: It means $0 upfront

❌ Not true—most plans still require a first payment

Myth 2: It’s cheaper

❌ Usually more expensive over time

Myth 3: Everyone qualifies

❌ Approval depends on your risk profile

How Insurance Companies Calculate Your Down Payment

Your initial payment depends on several factors:

- Your driving history

- Your credit score

- Your location

- Your coverage level

Higher-risk drivers usually pay more upfront, even with “low down payment” plans.

👉 The best way to reduce your upfront cost is to compare multiple quotes.

Quick Decision: Should You Choose No Down Payment?

- Need insurance immediately with little cash → choose no down payment

- Want the lowest total cost → pay in full

- Have limited savings → low upfront plan is safer

- Financially stable → upfront payment is better

👉 Still unsure?

Final Verdict: Is It Worth It?

- Need flexibility → no down payment is useful

- Want lowest cost → pay in full is better

👉 The best option depends on your financial situation

Frequently Asked Questions About No Down Payment Car Insurance

Can I Get No Down Payment Car Insurance After a DUI?

Drivers with a DUI can still obtain auto insurance coverage, but insurers usually require a higher upfront payment because they are considered higher risk. Comparing quotes from multiple companies may help reduce the initial payment required.

Can I Get No Down Payment Insurance With Bad Credit?

Some insurers may offer flexible payment plans to drivers with poor credit-related insurance factors. However, monthly premiums are often higher, making it important to compare both upfront costs and total policy costs.

Which Insurance Company Offers the Lowest Upfront Payment?

There is no single company that always offers the lowest upfront payment. The amount depends on your driving history, vehicle, state, coverage limits, and insurer pricing models. Comparing several quotes is usually the best way to find the most affordable option.

Conclusion

“No down payment car insurance” can help you start coverage quickly—but it’s not truly free.

Understanding the difference between upfront cost and total cost is the key to saving money.

Compare Car Insurance Quotes and Save Money

Don’t guess your rate—compare it.

👉 Prices vary widely based on your profile.

👉 Check your real price now:

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.