📉 Why Bad Credit Increases Insurance So Much

Many drivers are surprised by how much their insurance increases after their credit score drops.

The reason is that insurance companies don’t just look at your driving history. They also use statistical models that link financial behavior to risk.

Studies show that drivers with poor credit are statistically more likely to file claims. Because of this, insurers apply higher rates to offset that risk.

However, the important detail most people miss is that each company uses a different model. Some companies heavily penalize bad credit, while others apply only a small adjustment.

This is why two drivers with identical credit scores can receive completely different quotes from different insurers.

👉 The takeaway:

Your credit matters — but the company you choose matters even more.

If you have bad credit, you’re likely paying significantly more for car insurance than necessary.

In the U.S., drivers with poor credit can pay 70% to 100% higher premiums compared to those with good credit.

But here’s the part most people miss:

👉 Not all insurance companies treat bad credit the same way

Some insurers penalize heavily. Others barely do.

This guide shows you:

- The cheapest companies for bad credit drivers

- Real cost comparisons

- Proven strategies to reduce your premium fast

- How to choose the right insurer based on your situation

🚗 Quick Decision: Best Companies for Bad Credit

| Company | Best For | Why It Works |

|---|---|---|

| GEICO | Cheapest overall | Lower credit penalty |

| State Farm | Stable rates | Consistent pricing |

| Progressive | High-risk drivers | Flexible underwriting |

| Nationwide | Balanced option | Good discount system |

| Dairyland | Very poor credit | Easy approval |

⚡ Fast Action: Compare Quotes First (Most Important Step)

👉 The difference between companies can exceed $1,000/year

👉 Start here:

👉 Then double-check: Compare More Quotes – Backup Option

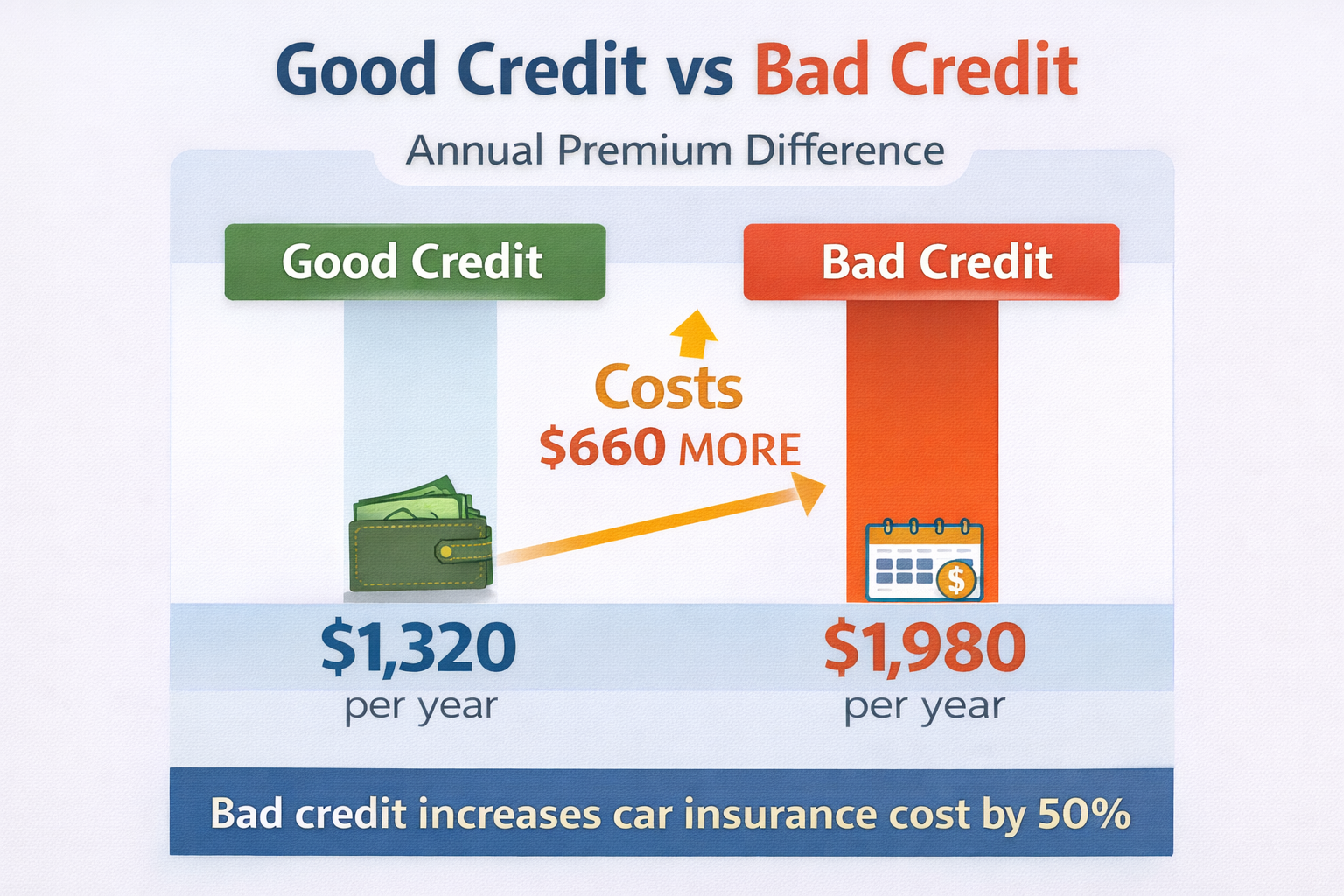

📊 How Much Bad Credit Increases Insurance Costs

Good vs Bad Credit Car Insurance Cost Comparison

Here’s what most drivers pay annually:

| Credit Score | Insurance Cost |

|---|---|

| 750+ | $1,200 |

| 700 | $1,400 |

| 650 | $1,700 |

| 600 | $2,200 |

| 550 or below | $2,500+ |

👉 That’s up to $1,300 more per year

📍 Cheapest Insurance for Bad Credit by State

Rates vary heavily depending on where you live.

| State | Good Credit | Bad Credit |

|---|---|---|

| California | $1,500 | $2,300 |

| Texas | $1,400 | $2,100 |

| Florida | $1,800 | $3,000 |

| New York | $1,700 | $2,700 |

👉 In high-cost states, bad credit hurts even more.

🏆 Best Cheap Car Insurance Companies (Detailed Breakdown)

GEICO – Best Overall Cheap Option

- Consistently lowest rates nationwide

- Less aggressive credit penalties

- Fast quote process

👉 Best for: Most drivers

State Farm – Best for Stability

- Smaller price jumps for bad credit

- Strong agent network

- Good bundling savings

👉 Best for: Long-term policy holders

Progressive – Best for High-Risk Profiles

- Accepts drivers with:

- Bad credit

- Accidents

- Tickets

- Usage-based discounts available

👉 Best for: Multiple risk factors

Nationwide – Balanced Choice

- Mid-level pricing

- Good add-ons

- Strong discount programs

👉 Best for: Balanced coverage

Dairyland – Last Resort Option

- Focuses on high-risk drivers

- Easier approval

- Higher base cost

👉 Best for: Very poor credit or rejections

👤 Real Case Study: $720 Annual Savings

Driver profile:

- Location: California

- Credit Score: 580

- No accidents

Initial quote:

- $2,280/year

After comparison:

- $1,560/year

👉 Saved: $720/year

👉 Conclusion:

The company matters more than your credit score.

🧠 Why Credit Score Affects Insurance

Insurance companies use a credit-based insurance score, which includes:

- Payment history

- Credit usage

- Length of credit

They believe:

👉 Lower credit = higher claim risk

👉 Learn more:

➡️ How Credit Score Affects Car Insurance Rates (2026 Guide)

🧠 How Insurance Companies Actually Evaluate Bad Credit Drivers

Most drivers assume that insurance companies simply look at their credit score and assign a price. In reality, the process is more complex.

Insurance companies use something called a credit-based insurance score, which is different from your traditional FICO score. While it still considers factors like payment history and credit utilization, it is specifically designed to predict the likelihood of filing an insurance claim.

For example, two drivers with the same credit score might receive completely different insurance quotes depending on how their credit profile is structured. Someone with a long credit history but a few missed payments may be treated differently from someone with a short credit history and high utilization.

This is why comparing quotes is critical. Each insurance company uses its own proprietary formula, meaning there is no universal pricing model.

In many cases, the difference between insurers can exceed $800 per year for the same driver profile. That gap has nothing to do with your driving ability — it is purely based on how each company interprets your credit data.

📉 Long-Term Strategy: Improving Your Credit to Reduce Insurance Costs

While switching companies can lower your insurance immediately, improving your credit score provides long-term savings.

Even a small improvement in your credit profile can lead to noticeable reductions in your premium. For example, moving from a credit score of 580 to 640 can shift you from a “poor” category to a “fair” category, which often results in lower rates.

The most effective ways to improve your credit include:

- Paying all bills on time

- Reducing credit card balances

- Avoiding new hard inquiries

- Keeping older accounts open

These changes don’t produce instant results, but within 3 to 6 months, many drivers begin to see improvements.

Insurance companies typically re-evaluate your profile at renewal, so maintaining better credit over time can significantly reduce your long-term costs.

⚠️ Common Mistakes Drivers with Bad Credit Make

Many drivers unknowingly overpay for insurance because they follow incorrect assumptions.

One of the biggest mistakes is staying with the same insurance company for too long. Loyalty rarely results in lower prices, especially for drivers with bad credit.

Another common mistake is choosing the lowest monthly payment instead of the lowest total annual cost. Monthly plans often include hidden fees that increase your overall expense.

Some drivers also avoid comparing quotes because they assume their credit will lead to rejection. In reality, most major insurers accept bad credit drivers, but pricing varies widely.

Finally, many people overlook discounts that could significantly reduce their premiums, such as bundling policies or enrolling in safe driving programs.

Avoiding these mistakes alone can save hundreds of dollars per year.

📉 How to Lower Insurance with Bad Credit

1. Compare Quotes (Highest Impact)

👉 This alone can save hundreds per year

2. Increase Deductible

- $500 → $1,000

- Save up to 30%

3. Use Driving Apps

State Farm Drive Safe

Progressive Snapshot

4. Bundle Insurance

Auto + home

Auto + renters

5. Pay in Full

👉 Save 5–10%

6. Drop Unnecessary Coverage

Older car?

→ Remove collision coverage

📊 How Fast Can You Lower Insurance with Bad Credit?

One of the biggest misconceptions is that lowering insurance requires improving your credit first.

In reality, you can reduce your premium immediately just by switching providers.

For example, many drivers see differences of $500 to $1,000 per year simply by comparing quotes across multiple companies.

Improving your credit score, on the other hand, is a longer process. It may take several months before your insurer updates your rate.

That’s why the smartest strategy is:

- Short term → switch companies

- Long term → improve credit

By combining both, you maximize your savings.

🧠 Advanced Strategies Most People Ignore

Pay-in-Full Discount

Paying your premium upfront can reduce total cost by 5–10%

Remove Unnecessary Coverage

If your car is older:

- Drop collision

- Drop comprehensive

Add a Low-Risk Driver

Adding a spouse with good driving history can reduce rates

⚖️ Decision Module: Which Company Should You Choose?

👉 Choose GEICO if:

- You want lowest price immediately

👉 Choose Progressive if:

- You have bad credit + violations

👉 Choose State Farm if:

- You want stable long-term pricing

👉 Choose Dairyland if:

- Others reject you

⚡ Best Strategy (Step-by-Step)

- Compare quotes

- Check second platform

- Pick lowest rate

- Adjust deductible

👉 Takes less than 10 minutes

📊 Monthly vs Pay-in-Full Cost Comparison

| Payment Method | Total Annual Cost |

|---|---|

| Monthly | $2,400 |

| Pay-in-Full | $2,200 |

👉 Savings: $200/year

❓ FAQ: Cheap Car Insurance for Bad Credit

Does bad credit always increase insurance?

In most states, yes. However, California, Hawaii, and Massachusetts restrict how credit is used.

Which company ignores credit the most?

GEICO and Progressive tend to be more forgiving compared to others.

Can I get cheap insurance with a 500 credit score?

Yes, but you must compare multiple companies. Some specialize in high-risk drivers.

How fast can I lower my rate?

Immediately — by switching providers.

🔗 Related Guides

- Cheap Car Insurance for Bad Credit (Full Guide)

- How to Lower Your Car Insurance Premium Fast (2026 Guide)

- Best Car Insurance for High-Risk Drivers (USA 2026)

🚀 Final Takeaway

Bad credit increases your insurance cost — but choosing the wrong company costs even more.

👉 The biggest mistake is not comparing quotes

🔥 Final Verdict

👉 Drivers with bad credit typically overpay by $500+ per year

👉 Fix that in 2 minutes:

👉 Want more options?

👉 Check Alternative Quotes Here

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.