Getting a DUI can double — or even triple — your car insurance cost.

Many drivers see their premiums jump from around $1,500/year to $3,000+ after a DUI conviction.

But here’s what most people don’t realize:

👉 Some insurance companies are far more forgiving than others

After a DUI, insurance rates can increase by 50% to 200% depending on your state and insurer.

However, not all companies price DUI drivers the same.

👉 Comparing quotes is often the fastest way to avoid overpaying after a DUI.

This guide shows you:

- The cheapest insurance companies after a DUI

- Real price differences

- How to lower your rate immediately

- Long-term strategies to reduce costs

🚔 What Is a DUI?

A DUI stands for Driving Under the Influence, which means operating a vehicle while impaired by alcohol or drugs.

In most U.S. states, a DUI is triggered when your blood alcohol concentration (BAC) reaches 0.08% or higher. Some states have even stricter rules for commercial drivers or underage drivers.

A DUI conviction typically results in:

- License suspension

- Fines and legal penalties

- Mandatory insurance filings (such as SR-22)

👉 Most importantly for drivers:

A DUI significantly increases your car insurance cost because insurers classify you as a high-risk driver.

DUI Insurance in California

California drivers may face:

- SR-22 filing requirements

- significantly higher premiums

- longer rate impacts

The exact increase depends on:

- insurer

- driving history

- ZIP code

- coverage level

🚗 Quick Decision: Best Cheap Insurance After DUI

| Company | Best For | Why It Works |

|---|---|---|

| Progressive | Best overall | DUI-friendly pricing |

| State Farm | Stability | Lower long-term increases |

| GEICO | Competitive rates | Strong online quotes |

| Travelers | Mid-range pricing | Balanced risk handling |

| Dairyland | High-risk drivers | Easy approval |

⚡ Fast Action: Compare Quotes First

👉 DUI pricing varies dramatically between companies

👉 Differences can exceed $1,500 per year for the same driver profile

👉 If you haven’t compared at least 3 providers, you are very likely overpaying.

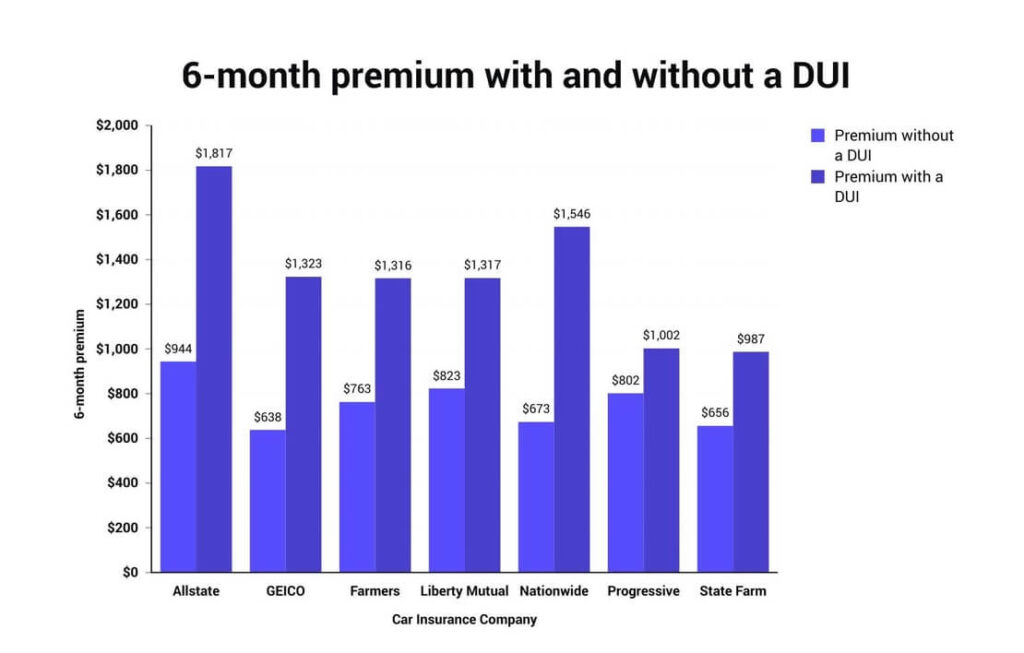

📊 How Much a DUI Increases Insurance Costs

Typical U.S. insurance costs:

| Driver Profile | Annual Premium |

|---|---|

| Clean record | $1,500 |

| DUI (Year 1) | $3,200 |

| DUI (Year 3) | $2,400 |

| DUI (Year 5) | $1,900 |

👉 A DUI can add $1,000–$2,000 per year

📍 Cheapest Insurance After DUI by State

Insurance laws vary by state, which impacts DUI pricing.

| State | Clean Record | After DUI |

|---|---|---|

| California | $1,700 | $3,500 |

| Texas | $1,500 | $3,000 |

| Florida | $2,000 | $4,200 |

| New York | $1,900 | $3,800 |

Why Rates Increase Differently

Insurance companies calculate DUI risk differently. Some insurers may increase premiums by 50%, while others may charge more than double the previous rate. This is why comparing quotes becomes especially important after a DUI conviction.

🏆 Best Cheap Car Insurance Companies After DUI (Detailed)

Progressive – Best Overall for DUI

- Known for high-risk drivers

- Accepts DUI cases easily

- Competitive rates

👉 Best for: Most drivers after DUI

State Farm – Best for Stability

- Lower long-term rate increases

- Strong local agent network

- Good bundling discounts

👉 Best for: Long-term savings

GEICO – Best for Fast Quotes

- Easy online process

- Competitive for some DUI cases

- Strong digital experience

👉 Best for: Quick setup

Travelers – Balanced Option

- Moderate pricing

- Good coverage options

👉 Best for: Mid-risk drivers

Dairyland – High-Risk Specialist

- Accepts severe cases

- Easier approval

👉 Best for: Multiple violations

👤 Real Case Study: Saving $1,050 After DUI

Driver:

- Age: 35

- Location: California

- DUI: 1 conviction

Quotes:

- Company A: $3,600/year

- Progressive: $2,550/year

👉 Savings: $1,050/year

👉 Key insight:

Not all insurers price DUI risk the same way.

A California driver paying approximately $150 per month before a DUI may see premiums rise substantially after a conviction. After comparing quotes from multiple insurers, the difference between the highest and lowest quote can be significant. Shopping around often becomes one of the most effective ways to reduce costs after a DUI.

🧠 Why Insurance Is So Expensive After DUI

A DUI signals higher risk to insurers for several reasons:

- Increased accident probability

- Legal liability exposure

- Higher claim costs

Insurance companies use risk models that heavily weight DUI history.

However, each insurer calculates risk differently.

👉 Some companies specialize in high-risk drivers

👉 Others aggressively penalize DUI

This creates large price differences.

DUI Insurance Strategy

Situation → What to Do

First DUI → Compare at least 3–5 companies

Multiple violations → Focus on high-risk insurers

Budget concern → Increase deductible + compare quotes

See available options from multiple providers. Takes about 2 minutes.

📉 Why Insurance Companies Penalize DUI So Heavily

Insurance companies rely on statistical risk models when pricing policies. A DUI is considered one of the strongest indicators of future claims because it reflects impaired judgment while driving.

From an insurer’s perspective, a driver with a DUI is more likely to be involved in an accident, file a claim, or cause damage that leads to higher payouts. This increased risk is priced directly into your premium.

However, not all insurers evaluate DUI risk the same way. Some companies specialize in high-risk drivers and apply more balanced pricing, while others significantly increase premiums to offset potential losses.

This is why comparing quotes is essential. The difference between insurers is often larger than the penalty itself.

📉 How to Lower Car Insurance After DUI

1. Compare Quotes (Most Effective)

👉 Biggest savings comes from switching companies

2. Increase Deductible

- $500 → $1,000

- Save up to 30%

3. Take Defensive Driving Course

- May reduce premiums

- Shows lower risk

4. Use Usage-Based Programs

- Track safe driving

- Earn discounts

5. Bundle Policies

- Combine auto + home/renters

- Save 10–25%

6. Maintain Clean Record

👉 Most important long-term factor

⚠️ SR-22 Insurance Requirements

After a DUI, many states require an SR-22 certificate.

This is not insurance itself — it’s proof that you carry minimum coverage.

Key points:

- Filed by your insurance company

- Required for 3–5 years

- Adds small fee (~$25–$50)

👉 Not all companies offer SR-22 easily

⏳ How Long It Takes to Recover from a DUI (Financially)

Most drivers assume that a DUI permanently affects their insurance, but that is not entirely true.

In general, the financial impact of a DUI is highest during the first one to three years. During this period, insurers consider you a high-risk driver and apply the highest premiums.

After three years, many insurance companies begin to reduce the impact of the DUI on your pricing, especially if you maintain a clean driving record.

By the five-year mark, the effect is often significantly reduced, and some insurers may treat you similarly to a standard driver.

This means that while the short-term cost increase is unavoidable, long-term savings are achievable through consistent safe driving and smart insurance choices.

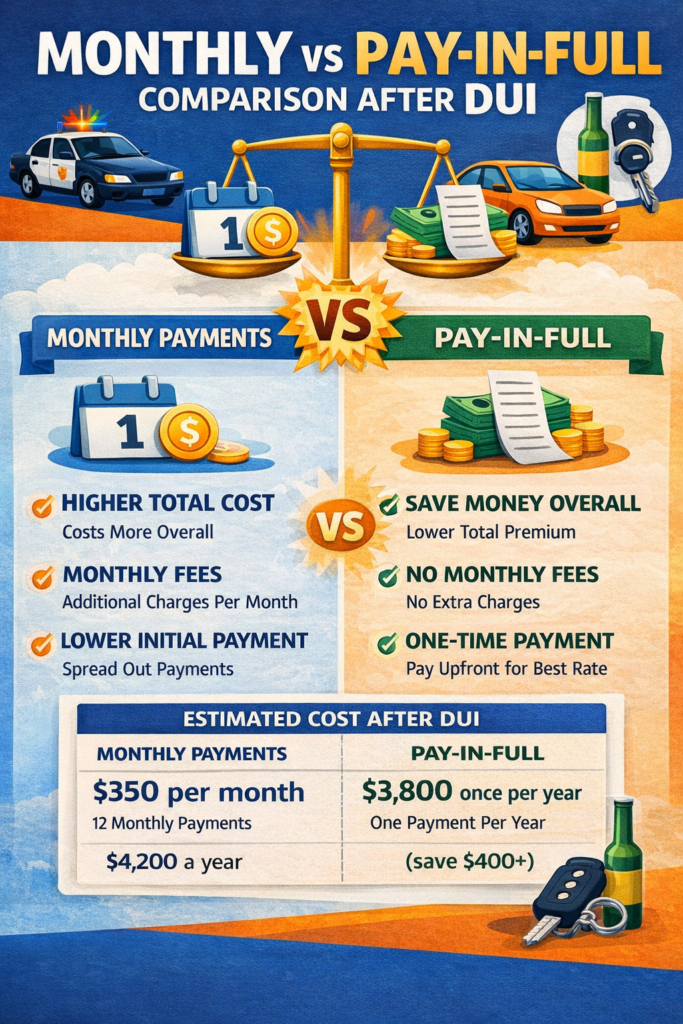

📊 Monthly vs Pay-in-Full Comparison

| Payment Type | Annual Cost |

|---|---|

| Monthly | $3,400 |

| Pay-in-Full | $3,100 |

👉 Savings: $300/year

📉 How Long a DUI Affects Insurance

| Time Since DUI | Impact |

|---|---|

| Year 1 | Very high |

| Year 3 | Moderate |

| Year 5 | Reduced |

| Year 7+ | Minimal |

👉 Most insurers consider DUI for 3–5 years

🧠 Advanced Strategy: Short-Term vs Long-Term Savings

Short-term:

- Switch companies

- Compare quotes

Long-term:

- Maintain clean record

- Improve driving profile

👉 Combine both for maximum savings

⚖️ Decision Module: Which Company Should You Choose?

👉 Choose Progressive if:

- You want lowest price immediately

👉 Choose State Farm if:

- You want stable long-term pricing

👉 Choose Dairyland if:

- You’ve been rejected elsewhere

👉 Choose GEICO if:

- You prefer online setup

❓ FAQ: Cheap Insurance After DUI

Can I still get cheap insurance after DUI?

Yes, but you must compare multiple providers.

Which company is cheapest after DUI?

Often Progressive, but varies by state.

Does DUI permanently increase insurance?

No — impact decreases over time.

How fast can I lower my rate?

Immediately by switching insurers.

🔗 Related Guides

- Cheap Car Insurance for Bad Credit

- How to Lower Car Insurance Premium Fast

- Best Car Insurance for High-Risk Drivers

Many drivers stay with their current insurer after a DUI and end up paying significantly more than necessary.

Rates can vary widely between companies for high-risk drivers.

👉 Checking multiple quotes is one of the few ways to reduce that impact.

🚀 Final Takeaway

A DUI increases your insurance — but choosing the wrong company costs even more.

👉 The biggest mistake is staying with the same insurer

🔥 Final Verdict:

👉 Drivers with DUI often overpay $1,000+ per year

👉 Fix that now:

Free to use. No obligation.

If you want to explore other options, you can also compare quotes here.

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.