Introduction

Finding cheap car insurance for bad credit can feel frustrating, especially when you already know your rate may be higher than someone else’s. Many drivers assume they have no choice but to accept an expensive quote. That is not true.

The reality is simple: bad credit can increase your premium, but it does not mean you have to overpay forever. Insurance prices vary a lot by company, state, coverage level, deductible, payment method, and driving profile. That means the cheapest option for one driver may not be the cheapest option for another.

This guide explains how bad credit affects car insurance, where the extra cost usually comes from, and what you can do right now to lower your premium without making risky coverage decisions. If you compare quotes the right way and avoid a few common mistakes, you can still find affordable coverage.

If you want to check your real price first, start here:

Does Bad Credit Really Affect Car Insurance Rates?

Yes, in many states, insurance companies use a credit-based insurance score when setting premiums. They do not look at your credit score for the same reason a bank does, but they often use it as one of many risk signals.

That means two drivers with similar cars and similar driving records can still receive different quotes if one has stronger credit and the other has weaker credit. The driver with poor credit often gets a higher rate.

This frustrates a lot of people because it feels unfair. But from the insurer’s point of view, they are pricing risk. Whether you agree with that or not, the practical takeaway is the same: if you have bad credit, you need to shop more aggressively and structure your policy more carefully.

If you want the full explanation of how this works, read our guide on how credit score affects car insurance rates.

Why Bad Credit Can Make Car Insurance More Expensive

Insurance companies do not usually say, “Your credit is bad, so we are charging you more.” Instead, the higher price gets built into the quote.

Here is what usually happens. A driver with poor credit may get fewer preferred pricing options, fewer billing advantages, and fewer discount combinations. In some cases, monthly installment plans also become more expensive, which raises the total annual cost even more.

Bad credit often hurts in three ways at the same time. First, the base premium may be higher. Second, the upfront payment may be larger. Third, the total cost can rise further if you choose monthly billing with fees.

That is why many drivers with bad credit focus on the wrong thing. They look only at the monthly number, when they should also compare the upfront payment, deductible, and total six-month or annual cost.

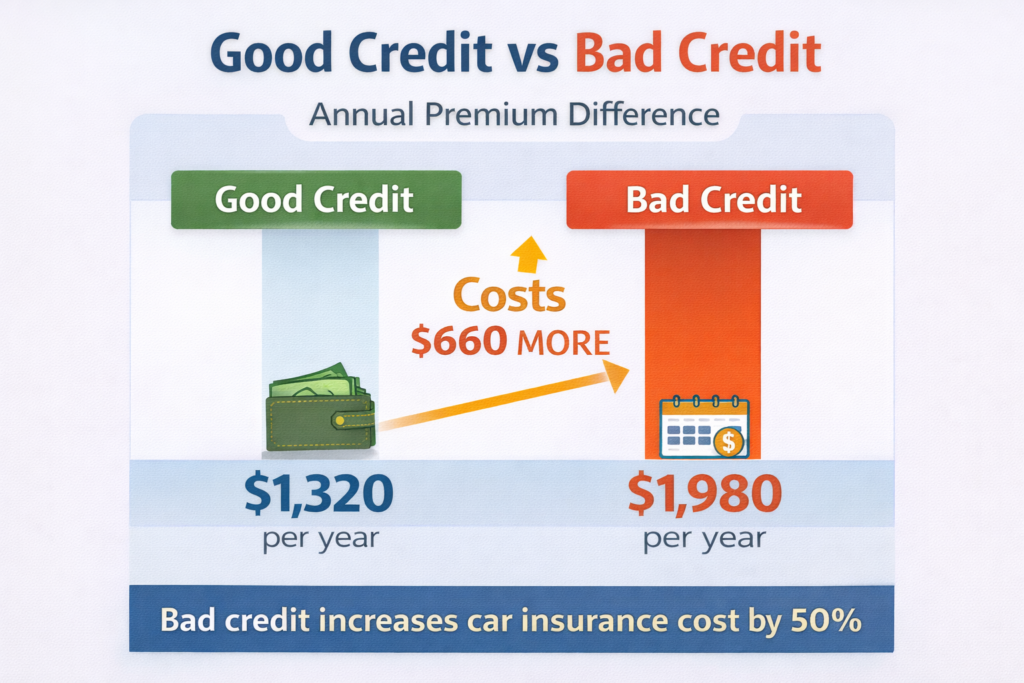

Real Example: Good Credit vs Bad Credit

Here is a simple example to show why this matters.

| Driver Profile | Monthly Premium | Six-Month Cost | Annual Cost |

|---|---|---|---|

| Good credit driver | $110 | $660 | $1,320 |

| Bad credit driver | $165 | $990 | $1,980 |

In this example, the driver with bad credit pays $660 more per year for similar coverage.

That difference is big enough to matter. It can affect whether you choose liability only, whether you raise your deductible, whether you pay monthly or in full, and whether you can afford stronger protection at all.

How bad credit can increase the total annual cost of car insurance.

Key Takeaway: How Much Bad Credit Really Costs

Drivers with bad credit can pay $500 to $1,000+ more per year for the same coverage.

👉 That means over 3 years:

👉 You could overpay $1,500–$3,000

👉 This is why comparing quotes is critical.

Can You Still Find Cheap Car Insurance with Bad Credit?

Yes, but you need the right strategy.

The first mistake is assuming the first quote is “the market price.” It is not. Car insurance is one of the most variable consumer financial products in the U.S. One company may rate you very aggressively because of your credit profile, while another may be noticeably cheaper because it weighs other factors more heavily.

The second mistake is chasing only the lowest monthly payment. A low monthly number can hide a high total cost, especially if the policy includes installment fees or a weak coverage structure that leaves you exposed after a claim.

The best mindset is this: you are not looking for “perfect” insurance. You are looking for the cheapest policy that still protects you well enough and does not trap you with a bad payment structure.

Decision Module 1: Should You Buy Minimum Coverage or More?

This is one of the biggest decisions for drivers with bad credit.

If your budget is very tight, minimum state-required coverage may look like the obvious answer. It is usually cheaper upfront and easier to keep active. But it also provides less protection. If you cause a serious accident, low liability limits can become a financial problem.

A fuller policy costs more, but it may save you far more if something goes wrong. This is especially important if you drive a newer car, commute long distances, or do not have much cash saved for emergencies.

A useful rule is this. If your main goal is simply to stay legal and keep the monthly bill low, minimum coverage may be the practical short-term choice. If you have a financed car, meaningful assets to protect, or higher daily driving exposure, going too cheap can backfire.

If you want to understand legal minimums first, read our guide on minimum car insurance requirements by state.

Ways to Lower Car Insurance Costs Even with Bad Credit

You still have several levers you can use.

First, compare quotes from multiple insurers. This matters more for drivers with bad credit than for drivers with average or good credit, because pricing spread is often wider.

Second, raise your deductible if you have emergency savings. A higher deductible usually lowers the premium. But do not do this unless you can truly afford the deductible after an accident. If you are still deciding, read deductible vs premium to understand the tradeoff.

Third, avoid unnecessary extras that do not fit your real needs. Rental reimbursement, roadside add-ons, and other optional items are not always bad, but they should be chosen intentionally.

Fourth, ask about discounts. You may still qualify for safe-driver, multi-policy, automatic payment, paperless billing, defensive driving, or vehicle safety discounts.

Fifth, compare the total cost of paying monthly versus paying upfront. In many cases, paying in full reduces the overall price. Monthly billing is easier on cash flow, but it can cost more over time.

Decision Module 2: Should You Raise Your Deductible?

This is where many drivers with bad credit can save money, but also where many make mistakes.

If you move from a $250 deductible to a $500 or $1,000 deductible, your premium may drop. That sounds good. But after a claim, you must pay more out of pocket before insurance covers the rest.

So the question is not just “Will this lower my rate?” The better question is “Can I actually pay this deductible without creating a bigger financial problem?”

If you have emergency savings and rarely file claims, a higher deductible is often the better financial choice. If you live paycheck to paycheck or would struggle to cover a repair bill, a lower deductible may be safer even if the premium is higher.

Quick rule: a deductible only saves you money if you can comfortably afford it when something happens.

Quick Decision: What Is the Best Option for Most Drivers with Bad Credit?

Use this simple guide.

If your budget is extremely tight and you need immediate legal coverage, choose a lower-cost liability policy and compare multiple quotes right away.

If you can afford a moderate upfront payment and have some emergency savings, choose stronger coverage with a higher deductible to reduce the premium.

If you are paying monthly and the total cost is high, check whether paying in full would save enough to matter.

If your quote looks unusually expensive, do not assume all companies are the same. Shop again.

For most drivers with bad credit, the best path is:

compare widely, avoid overinsuring, keep meaningful liability protection, and use a deductible you can truly afford.

Cheap Insurance vs Bad Insurance: Know the Difference

Cheap insurance is not always bad insurance. Bad insurance is a policy that looks cheap until you need it.

A very low premium can come from low liability limits, missing coverages, a deductible you cannot afford, or a payment structure loaded with fees. That is why the smartest shoppers do not compare price alone. They compare value.

For example, one quote may be $18 cheaper per month but come with much lower liability limits. Another may cost slightly more but include a better structure, fewer fees, and better long-term value.

That is why you should compare the same general protection level across quotes when possible. Otherwise, you are not making a real apples-to-apples comparison.

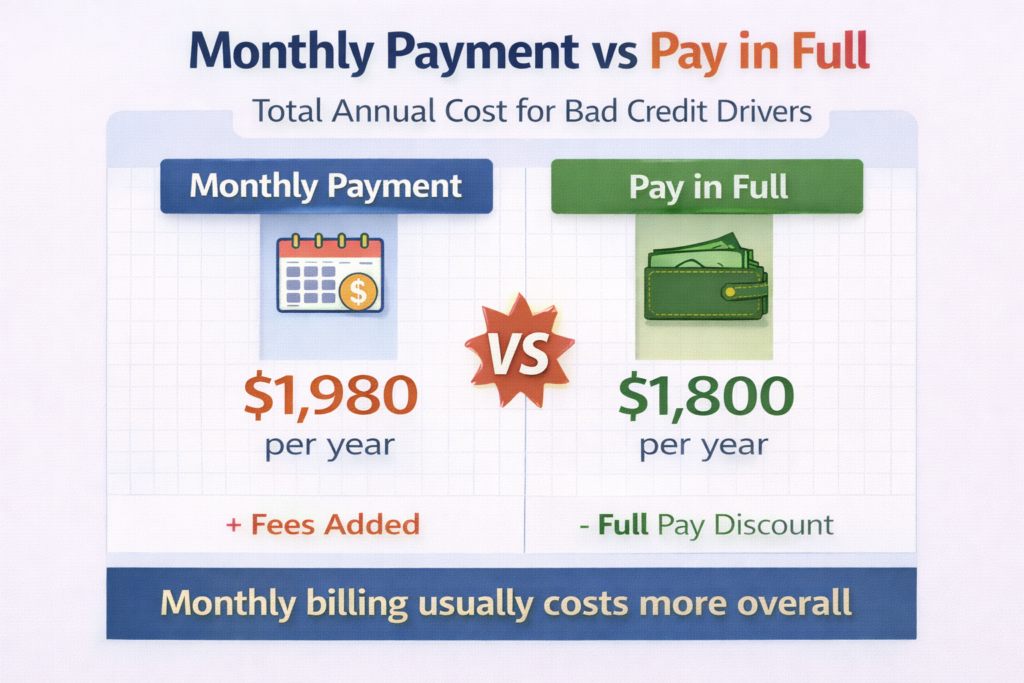

Monthly Payment or Pay in Full?

Drivers with bad credit often prefer monthly payments because the first bill feels easier to manage. That makes sense from a cash-flow standpoint. But monthly billing often raises the total cost.

Some insurers charge installment fees. Others provide a paid-in-full discount that monthly customers do not get. Over a six-month policy term, that difference can become meaningful.

If you can afford to pay upfront, paying in full is often the cheaper option overall. If not, monthly payments may still be the right practical choice, but you should compare the real total cost before deciding.

This is especially important if your quote already looks expensive due to credit. Saving even a small amount on billing structure can help.

Why paying monthly can cost more than paying in full.

Companies, Quotes, and Shopping Strategy

There is no single insurer that is always cheapest for every driver with bad credit. That is why shopping strategy matters more than brand assumptions.

When comparing quotes, keep the structure as consistent as possible. Use the same car, address, deductible, and coverage level. Then compare what changes. Look at the monthly premium, the upfront payment, and the total policy cost.

Do not rely on one quote, one ad, or one “best company” list. Your actual rate depends on your own profile. A company that is great for one driver may be expensive for another.

The smartest approach is to gather several quotes in one sitting and make the decision from there.

Start here:

Common Mistakes Drivers with Bad Credit Should Avoid

One common mistake is buying the first policy that gets approved. Approval is not the same as value.

Another mistake is choosing the lowest monthly price without noticing the deductible or payment fees.

A third mistake is dropping useful protection too aggressively. Saving money matters, but saving the wrong way can be costly later.

A fourth mistake is assuming credit is the only thing that matters. It matters, but so do mileage, vehicle type, ZIP code, age, coverage limits, and driving history. That is why quote shopping works.

A fifth mistake is not reviewing the policy again after six months or after a credit improvement. Even a modest score improvement can help, and market pricing changes over time.

Best Strategy for Drivers with Bad Credit

If you want the lowest cost possible:

- Compare at least 3–5 quotes

- Choose a higher deductible (if affordable)

- Avoid unnecessary add-ons

- Pay in full if you can

👉 This combination gives you the maximum savings

👉 Start here:

Final Verdict

Yes, bad credit can make car insurance more expensive. But it does not mean you are stuck with a terrible deal.

You can still find cheap car insurance for bad credit if you compare quotes carefully, keep the right level of coverage, choose a deductible that matches your savings, and pay attention to the total cost instead of just the monthly number.

For most drivers in this situation, the winning formula is simple: shop harder, compare smarter, and structure the policy around your real budget instead of fear.

Sources

Consumer Financial Protection Bureau (CFPB)

Insurance Information Institute (III)

Compare Car Insurance Quotes and Save Money

If you want the fastest way to see what you may actually pay, compare quotes now and look for the best balance between premium, deductible, and protection.

About the Author

SaveMoneyInUSA Editorial Team researches car insurance, personal finance, banking products, and money-saving strategies for consumers in the United States.

Learn more about our Editorial Team.

Disclaimer

SaveMoneyInUSA is an independent informational website and is not an insurance company, broker, or agent.

Some links may be affiliate links. We may receive compensation from partners at no additional cost to users.

Insurance rates, coverage options, and eligibility vary by provider and individual circumstances.

This content is provided for educational purposes only and should not be considered insurance, legal, or financial advice.